Floating Product Market Set to Rebound in 2021- Updated Market Report Released

In its latest quarterly Floating Production Systems Report, Energy Maritime Associates (EMA) reviews the market for Floating Production Systems, including:

• 296 Production Units and 107 FSOs in operation

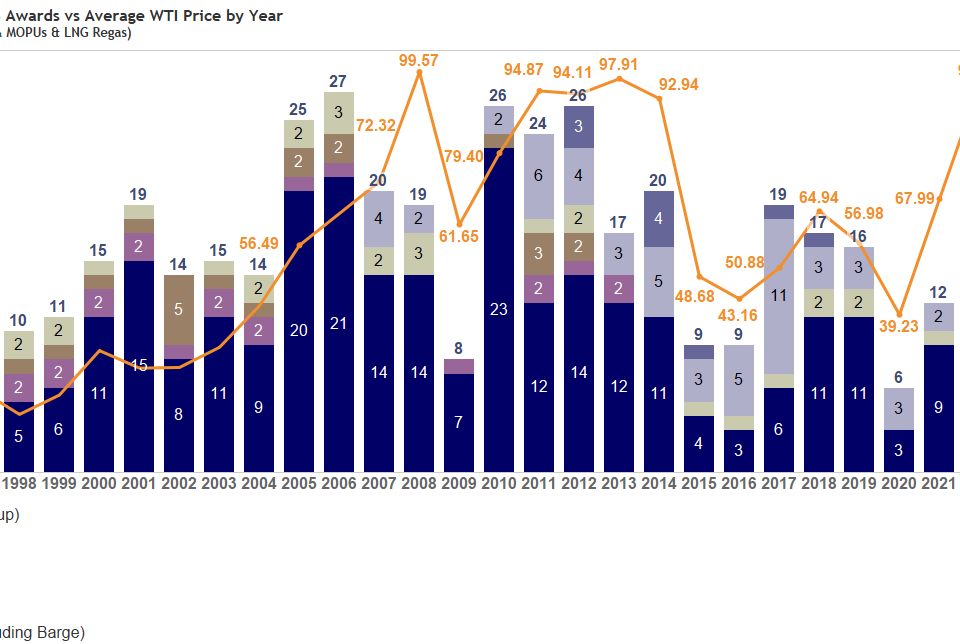

• 7 Major awards in 2020: 3 FPSOs, 3 FSRUs and 1 MOPU

• 14 Deliveries scheduled for 2021

• 53 Production units, including 42 FPS, 8 FSOs and 5 MOPUs on order

• 202 Projects in pipeline – up two from last quarter

2020 saw a record low number of awards due to the oil price crash and COVID-19 impacts. The year was off to a strong start with seven awards in the first two months of 2020, but this came to a sudden half with crashing oil prices in March.

Results compiled from our recent Global Industry Sentiment Survey confirm that after four years of steady improvement, COVID-19 and an oil price collapse darkened the global FPS industry sentiment in 2020. However, the expectation is for a more rapid rebound than the last cycle, with many companies still managing record backlogs.

The floating production market remains the brightest spot in the offshore industry today, including growing excitement in the nascent floating wind sector. Offshore development costs remain low, fueled by excess drilling and subsea capacity. However, field operators are under increasing scrutiny from investors to balance capital investment, returns, and ESG issues. Activity levels are expected to improve in 2021-2022, but at a measured pace as operators and contractors keep close watch on spending, resources, and execution risk.

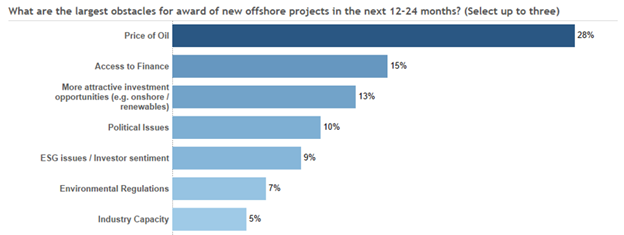

For the seventh year in a row, the price of oil was identified as the greatest obstacle to offshore project growth. This year, the impact was extreme, as 28% of respondents cited oil price, up from 19%.

Fig 1. Greatest growth obstacles to new project awards over the next 12-24 months.

In addition to challenges for investment from renewables, there is a growing push to reduce investment in hydrocarbons. In-line with this trend, ESG issues / investor sentiment ranked in fifth place, followed by environmental regulations.

Upcoming Webinar

Join EMA Managing Director David Boggs on January 21 for a live discussion on the status of projects on order, the forecast for new awards, as well as highlights from our annual industry survey. This webinar is hosted by Offshore Magazine and Chief Editor David Paganie.

EMA provides accurate and dependable quarterly reports for the Floating Production Sector.

Clients tell us that our reports are the best source for information about upcoming developments.

New Report Contains Results of 8th Annual Global Industry Sentiment Survey.

In its latest quarterly Floating Production Systems Report, Energy Maritime Associates (EMA) reviews the market for Floating Production Systems and discusses the results of the 8th Annual Global Industry Sentiment Survey.

{kind=link}

{kind=link}