NEWS RELEASE – October 8, 2019

Energy Maritime Associates Releases Updated Floating

Production Systems Report

– Wave of new contract awards expected in Q4 2019

SINGAPORE – In its latest quarterly Floating Production Systems Report, Energy Maritime Associates (EMA) reviewed the market for Floating Production Systems, including:

- 300 Production Units and 104 FSOs in Operation

- 225 Projects in the Planning Pipeline

- 46 Production Units, 8 FSOs and 5 MOPUs on Order

- 49 Available Units (26 FPSOs, 7 Semis, 6 MOPUs, 4 FSRUs, 3 FSOs, 1 Barge, 1 Spar, 1 TLP)

After a strong start in the first half of the year, the pace of orders slowed down with only four announced in Q3 (1 FPSO, 1 FSRU, and 2 LNG FSOs). This brings the total number of units awarded in 2019 to thirteen: 6 FPSOs, 3 FSRUs, 2 FSOs (LNG), 1 Semi, 1 MOPU.

However, 27 projects that are likely to reach FID in the next 12 months, including many that have completed tendering and are just pending final FID/formal announcement. We expect a surge of orders before year end, particularly from Petrobras, which has five projects in the tender process. EMA expects up to six additional FPSO awards in the next three months.

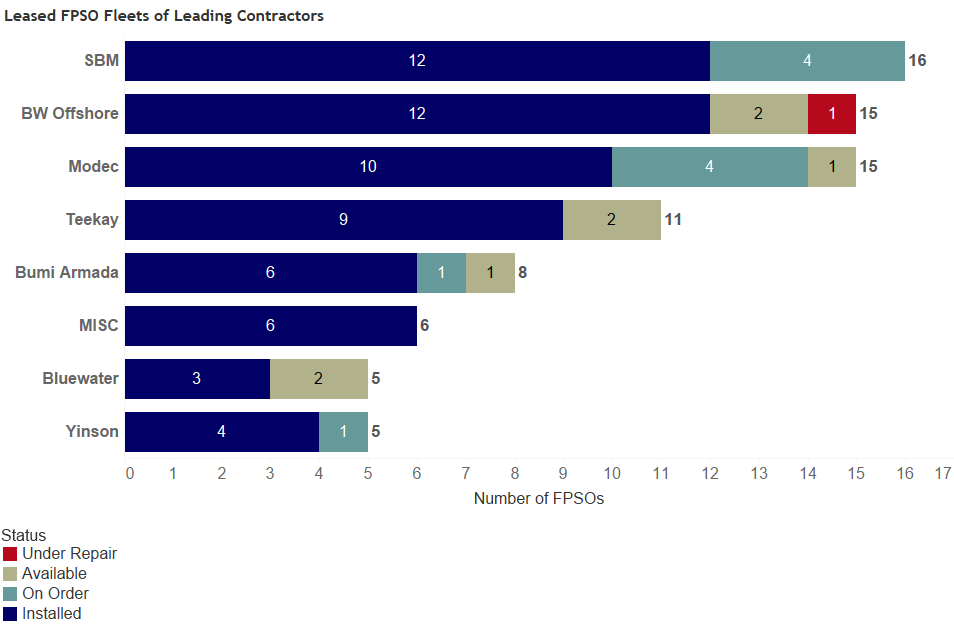

The orderbooks of contractors are filling up, with leading companies taking on multiple projects. Modec and SBM each have four FPSOs on order. There have been a range of responses to this increase in activity:

1.) Long-term agreements

a. ExxonMobil & SBM (September 2019), expected to cover requirements for three more FPSOs in Guyana

2.) New entrants

Kvaerner to expand: “We believe that we are able to offer one of the world’s best production lines for advanced FPSOs, focusing on secure execution within agreed quality, time and budget. We aim to win and execute a series of FPSO projects after Johan Castberg.”

3.) Capacity constraints/Cost inflation

a. Contractors have reported constraints in certain areas, particularly for yard capacity and experienced personnel.

b. Costs are starting to increase for in-demand, skilled roles

Figure 1. Leased FPSO Fleets of Leading Contractors, (c)EMA 2019

We will analyze these issues and more on the future of the industry in our next publication, which is the Floating Production Outlook Report (2020-2024). The report will be released in early December and contains a detailed analysis of the FPS market over the next five years.

About Energy Maritime AssociatesThe Floating Production Systems Report is a must read for anyone requiring trustworthy analysis of the FPSO sector to effect better decision making, assess business risk, and provide insight into project alternatives.

Since 1996, EMA has been providing independent, expert analysis of the FPSO market with an unbiased view. We pride ourselves on the accuracy of information provided built through an extensive network of industry contacts, and our depth of knowledge in floating production. Trusted by more than 200 clients worldwide, EMA serves the entire FPSO market including E&P companies, service providers, capital investment firms, and asset and facility owners.

EMA will be participating in the following industry events:

Please contact us to schedule a meeting to discuss how we can answer your questions about the floating production sector.

For further information contact:

Energy Maritime Associates Pte Ltd

2020 April FPS Quarterly Report: Table of Contents

I. Current and Planned Floating Production Systems

Recent orders

Recent deliveries

What’s now being built

Trend in order backlog

Composition of order backlog

Current fabrication and conversion activity

Floater projects planned or under study

Floating production database

II. Recent Developments

Floater Prospects in the Appraisal Stage

NEW Trinidad & Tobago North (Trinidad)

NEW Saasken (Mexico)

NEW Maka (Suriname)

Floater Prospects in the Planning Stage

NEW Agogo (Angola)

Cameia & Golfino (Angola)

NEW Lamu Export Terminal (Kenya)

Browse (Calliance / Brecknock, Torosa) (Australia)

NEW Carcara North (Brazil)

Parque dos Doces (Brigadeiro) (Brazil)

Bay du Nord (Newfoundland)

Trion (Mexico)

Aphrodite (Cyprus)

NEW Peon (Norway)

Wisting (Norway)

Gehem/Gendalo (Indonesia Deepwater Development) (Indonesia)

Geronggong / Jagus (Brunei)

NEW MASA redevelopment (Malaysia)

NEW Salam / Patawali (Malaysia)

Singa Laut / Kuda Laut (Indonesia)

NEW Liuhua 12-04 (China)

Floaters in the Bidding or Final Design Stage

Blk 31 SE - PAJ (Angola)

Etinde (Cameroon)

Pecan (Ghana)

Scarborough (Australia)

Atlanta/Olivia (Brazil)

NEW Buzios 6 (Brazil)

Deep Waters Sergipe (Barra / Farfan) (Brazil)

Gato do Mato (Brazil)

Mero 3 (Brazil)

Mero 4 (Brazil)

Neon / Goia (ex-Echidna / Kangaroo) (Brazil)

North Platte (U.S.)

Shenandoah (U.S.)

Zama (Mexico)

Cambo Hub (U.K.)

Marigold / Sunflower (U.K.)

NEW Forel (Indonesia)

NEW G1 FSO (Thailand)

Lac Da Vang (Vietnam)

Limbayong (Malaysia)

Nam Du / U Minh (Vietnam)

Cancelled FPS Projects

Gohta / Alta (Norway)

Al Shaheen FSO Replacement (2 units) (Qatar)

New Orders

Sangomar FPSO (Senegal)

Ana Neri FPSO (Brazil)

Anita Garibaldi MV33 FPSO (Brazil)

Bacalhau FPSO (Brazil)

Whale Semi SEMI (US)

Acajutla FSRU (El Salvador)

Bayan MOPU (Malaysia)

Al Khaznah FSO (LNG) (India)

Fast4Ward #4 & #5 (Speculative Hull) FPSO

Systems on Order

Gimi FLNG and Tortue FPSO (Mauritania)

Barossa FPSO (Australia)

FPSO Miamte MV34 (Mexico)

Maersk Inspirer MOPU (Norway)

Prosperity FPSO (Guyana)

Maran Speculative (Hull 2477) FSRU (Pakistan)

Prem Pride FSO (India)

Systems Recently Completed

Abigail-Joseph (ex-Allan) FPSO (Nigeria)

ELI Akaso FSO (Nigeria)

Karmol LNGT Powership Africa FSRU (Mozambique)

P 70 FPSO (Brazil)

MTC Ledang FPSO (Malaysia)

PFLNG Dua FLNG (Malaysia)

Nan Hai Shi You 121 FSO (China)

Dukhan FSO (LNG) (India)

Existing Systems

Kwame Nkrumah FPSO (Ghana)

Raroa FPSO (New Zealand)

Capixaba FPSO (Brazil)

Golar Nanook FSRU (Brazil)

OSX 3 FPSO (Brazil)

Terra Nova FPSO (Canada)

BW Pioneer FPSO (WR 206)

Enquest Producer FPSO (U.K.)

Petrojarl Banff FPSO and Apollo Spirit FSO (U.K.)

Petrojarl Foinaven FPSO (U.K.)

PTSC Lam Son FPSO (Vietnam)

Golar Igloo FSRU (Kuwait)

Available Systems

Armada Claire FPSO

BW Opportunity (ex-Cidade de Sao Mateus) FPSO

Dhirubhai 1 FPSO

Gimboa FPSO

Northern Endeavor FPSO

P 33 FPSO & P 37 FPSO

Umuroa FPSO

Voyageur Spirit FPSO

Cancelled Orders

Pecan FPSO (Ghana)

ONGC MOPUs (Sagar Pragati, Sagar Laxmi, Sagar Samrat)

Recycled Units

Nan Hai Fa Xian FPSO (China)

Nan Hai Sheng Kai FSO (China)

Angsi FSO (Malaysia)

Cendor FSO (Malaysia)

Energy 1 (ex Soraya) MOPU (Thailand)

Perintis FPSO (Malaysia)

III. Underlying Market Drivers

Highlights

Oil Price Forecast and Market Developments

Economic Activity and Oil Demand

Supply: Capex Slashed Across the Board After OPEC+ Last Waltz In Vienna

OPEC

US Onshore

Global Upstream Spending Slashed At Least 20%

Offshore Drilling Contracts Terminated

IV. Industry Activity & Analysis

COVID-19 & Oil Price Crash Impact on Existing Orders

Likely Awards in Next Year Drop by 75%

Teekay Offshore Renamed Altera Infrastructure

Appendix I: Projects in Planning Pipeline

Africa

Australia

Brazil

Canada

Caribbean

Gulf of Mexico

Mediterranean

North Sea

South America (excluding Brazil)

Southeast Asia

China

Southwest Asia and Middle East

Appendix II: On Order FPS Units

BARGE 2 units

FPSO 23 units

FLNG 3 units

FSRU 13 units

SEMI 7 units

FSO 8 units (3 Oil, 5 LNG)

MOPU 3 units

Appendix III: Installed and Available FPS Units

FPSO: 171 units

BARGE: 9 units

FLNG: 5 units

FSRU: 27 units

LNG REGAS: 7 units

SEMI: 39 units

SPAR: 21 units

TLP: 27 units

FSO: 109 units (103 Oil, 6 LNG)

MOPU: 18 units

Available Units

Appendix IV: Historical Installed FPS Units

2020 April FPS Quarterly Report: List of Illustrations

- Fig 1. Total Units by FPS Type

Fig 2. Total FPSOs by Status

Fig 3. Available Units by Type and Year Idle

Fig 4. Units Awarded by Quarter

Fig 5. Units Awarded by Capex

Fig 6. FPS Units Awarded Since Q4 2019

Fig 7. FPS Awards in Relation to Oil Price

Fig 8 FPS Units Delivered in 2019

Fig 9. FPS Units On Order by Hull Type

Fig 10. FPS Units On Order by Contract Type (Lease/Own)

Fig 11. Map of FPS Units on Order

Fig 12. Order Backlog for FPS Units

Fig 13. Orderbook 2008-2019

Fig 14. Distribution of Units on Order by Yard

Fig 15. Projects in Planning Pipeline by Region

Fig 16. Projects in Planning Pipeline by Region-LNG&Non-LNG

Fig 17. Deepwater and Ultra Deepwater Projects by Region

Fig 18. Projects in Bidding and Final Design Stage by Region and Water Depth

Fig 19. Projects in Planning Stage by Region and Water Depth

Fig 20. Projects in Appraisal Stage by Region and Water Depth

Fig 21. Map of FPS Units

Fig 22. Table of Production and Storage Floaters by Type and Region

Fig 23. FPSO by Status and Region

Fig 24. FSO by Status and Region

Fig 25. FSRU by Status and Region

Fig 26. FLNG by Status and Region

Fig 27. SEMI by Status and Region

Fig 28. SPAR/TLP by Status and Region

Fig 29. Brent has collapsed

Fig 30. GDP Demand Changes

Fig 31. Jet fuel consumption

Fig 32. Global Oil Supply Growth

Fig 33. Global Oil Demand-Supply Balance

Fig 34. OPEC Crude Production Forecast

Fig 35. US Land Rig Count vs WTI Price

Fig 36. Average US LTO Production

Fig 37. Selected Companies Capex Cut

Fig 38. Mobile Drilling Rig Outstanding Requirements

Fig 39. Mobile Drilling Rig Charter Rates vs Utilisation

Fig 40. COVID-19 Impact on Units on Order - FPSOs

Fig 41. COVID-19 Impact on Units on Order - FSO, MOPU, Barge, SEMI

Fig 42. COVID-19 Impact on Units on Order - LNG Units

Fig 43. COVID-19 Impact on Likely Awards - FPSOs

Fig 44. COVID-19 Impact on Likely Awards - Non-FPSOs

Fig 45. FPS Units On Order Summary

Energy Maritime Associates Releases Updated Floating Production Systems Report

In its latest quarterly Floating Production Systems Report, Energy Maritime Associates (EMA) reviewed the market for Floating Production Systems